Copper, Gold, Demand and Supply

Amid the green energy push, look for balance...

Two commodities have emerged as pivotal players as geopolitical tensions

have escalated, influencing

global financial markets: gold and copper, writes Frank Holmes at US Global

Investors.

These metals are not merely survivors of market

volatility but are thriving, charting

a course that I believe savvy investors would be wise to monitor.

As I've said

countless times before, gold

has long been considered a store of value in turbulent times, and now is no exception. Prices are near

all-time highs, reflecting its

enduring appeal during periods of uncertainty.

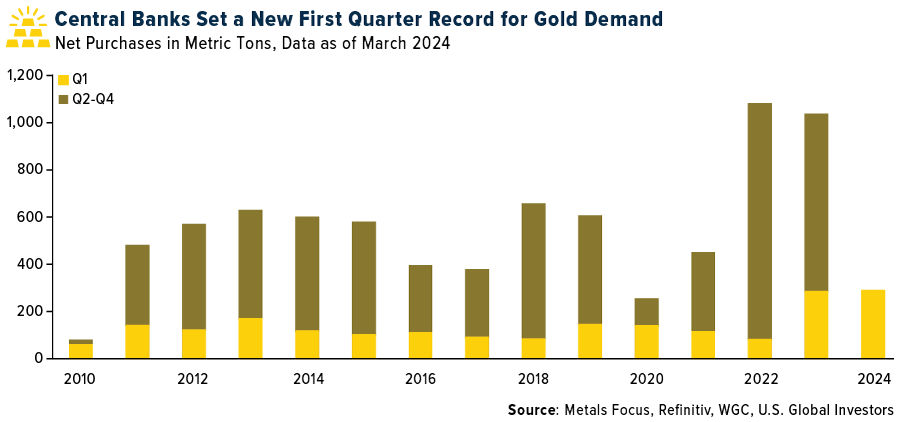

Central banks, particularly in

emerging markets, are

increasing their gold reserves. The first quarter of 2024 saw institutions purchase a record 290 tons of

gold, according to the World

Gold Council (WGC). This unprecedented amount highlights a strategic shift toward the metal as a reserve

currency and away from the US

Dollar.

While gold secures its

position as a safe haven, copper is making headlines for different reasons. Often referred to as "Dr.

Copper" for its ability to

predict economic trends due to its widespread industrial applications, copper has also seen a

significant price increase in recent

days. The industrial metal climbed to a two-year high, supported by strong global economic activity,

particularly surging demand

driven by energy transition technologies like electric vehicles (EVs), wind and solar.

The global copper

market is tightening. Production challenges, such as stoppages and declining ore grades in major South

American producers, are

anticipated to limit supply growth this year, though rebound is expected in 2025.

Despite these challenges,

the demand for copper continues to grow, fueled by its critical role in green energy solutions. The

International Copper Association

(ICA) forecasts that copper demand will increase from 28.3 million metric tons in 2020 to 40.9 million

metric tons by 2040, with a

compound annual growth rate of 1.85%.

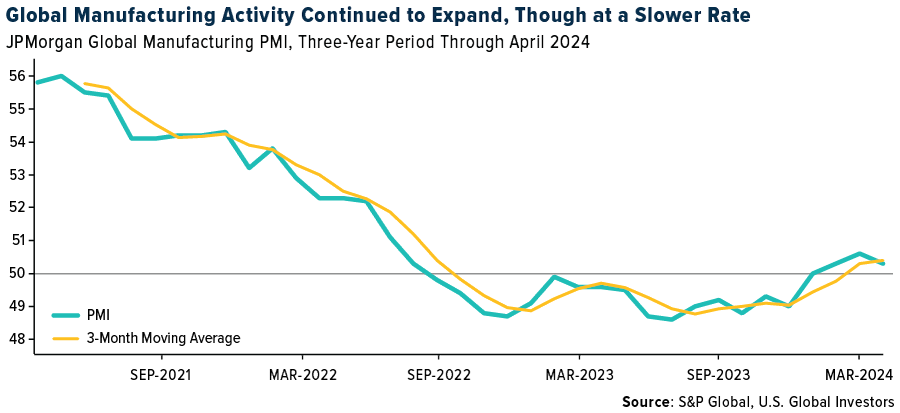

The global manufacturing sector provides

further insights. The JPMorgan

Global Manufacturing PMI saw a slight decline to 50.3 in April from a 20-month high of 50.6 in March,

but it remains above the neutral

mark, indicating expansion. This resilience in manufacturing suggests a sustained demand for industrial

metals, reinforcing the

bullish outlook for copper.

Rising input costs

and selling prices within the

manufacturing sector point to building price pressures, likely contributing to inflation concerns. Such

economic indicators are

critical for investors to consider as they assess the potential impacts on commodity prices and

investment returns.

The shift toward a low-carbon economy is not just a policy preference but a potential

investment theme. BloombergNEF

reports that global investment in the energy transition reached a staggering $1.8 trillion in 2023,

nearly doubling from 2020 levels.

Such investments, particularly in regions like Europe, the Middle East and Africa (EMEA), are expected

to drive further demand for

copper, given its essential role in electrification and renewable energy infrastructures.

For

investors, the implications of these trends are clear. Gold remains a critical asset in any diversified

portfolio, especially for

those seeking to hedge against geopolitical risk and potential inflation. Persistently strong demand

from central banks further

supports the investment case for the yellow metal. I always recommend a 10% weighting, with 5% in

physical gold (bars, coins,

jewelry), the other 5% in high-quality gold mining stocks, mutual funds and ETFs.

Not to be outdone, copper

presents a compelling growth story tied to the global economic recovery and the transition to green

energy. With the expected increase

in demand and current supply constraints, prices may continue to rise, presenting a valuable opportunity

for investors.

Past performance does not guarantee future results. All opinions expressed and data

provided are subject to change

without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s)

above, you will be directed

to a third-party website(s). US Global Investors does not endorse all information supplied by this/these

website(s) and is not.

Email

us

Email

us